Hurricane Car Damage Insurance Florida: Claims & Repairs Guide

Florida hurricanes strike fast and leave cars battered—dented by hail, scratched by wind-driven debris, flooded from storm surge, or structurally twisted. If you’re searching “hurricane car damage insurance Florida,” you’re likely staring at your damaged ride after events like Helene or Milton, wondering: Does insurance cover hurricane car damage Florida? The short answer? Yes, but only if you have comprehensive coverage—Florida’s PIP and PD liability minimums do not cover your own vehicle.

We’ve seen it firsthand at Pro Car Auto Body Shop in Pompano Beach. In our 10+ years serving Florida drivers through brutal storm seasons, hundreds have walked in from Miami flood zones, Orlando wind damage, Tampa hail storms, or Jacksonville debris hits with the same questions. “Is my hail-dented hood covered?” “What about hidden flood damage?” “Will this total my car?”

The reality: Comprehensive coverage handles hurricane flood damage car insurance Florida claims for wind, hail, flying debris, falling objects, and even flood—but deductibles apply (often $500–$2,500), and insurers scrutinize everything. No comprehensive? You’re footing the full bill. Plus, myths abound: Claims won’t hike rates for these “acts of God,” you can choose any licensed shop per Florida Statute §626.9743, and supplements for hidden damage are common.

This guide breaks it all down—step-by-step Florida hurricane vehicle damage claim process, total loss thresholds, repair vs. replacement pros/cons, and how certified shops like ours maximize your settlement. From South Florida to the Panhandle, we serve all Florida. Need help now? Call (561) 372-4547 or email info@procarautobodyshop.com for a free assessment at 1705 Dixie Hwy, Pompano Beach, FL 33060. Let’s get your car covered and road-ready.

Does Insurance Cover Hurricane Car Damage in Florida?

Florida’s hurricane season (June–November) wreaks havoc on vehicles. But coverage hinges on your policy.

Liability and PIP won’t help. Florida mandates Personal Injury Protection (PIP) and Property Damage (PD) liability—great for medical bills or others’ property, but they exclude your own car.

Comprehensive is key. This optional coverage protects against non-collision perils like hurricanes. It typically includes:

- Hail dents and cracks

- Wind-blown debris scratches or impacts

- Falling trees/branches

- Flooding from storm surge or heavy rain

Without it, zero payout. About 80% of Florida drivers carry comprehensive, per recent IIABA data—but confirm yours.

Real example: After Milton, a Palm Beach client thought her flooded SUV was uncovered. Our detailed water damage assessment proved submersion under comprehensive, securing a $12K settlement after supplements.

Comprehensive Coverage for Hurricane Car Florida: What It Covers

Comprehensive shines in storms. Here’s what it handles:

| Hurricane Damage Type | Covered Under Comprehensive? | Examples & Notes |

| Hail | Yes | Dents, chipped glass; paintless dent repair (PDR) often cheapest fix. |

| High Winds | Yes | Scratches, loose panels; frame straightening if structural. |

| Flying Debris | Yes | Dents, cracks from branches/signs; common in Broward/Tampa. |

| Flood/Water | Yes (if sudden/accidental) | Interior corrosion, electrical shorts; hidden mold needs supplements. |

| Falling Objects | Yes | Trees, roofs; total loss likely if frame totaled. |

| Vandalism/Looting | Sometimes | Post-storm break-ins; check policy exclusions. |

Deductibles apply—pay first, insurer covers rest. No comprehensive? Shop Insurance Claim Assistance for guidance.

What Comprehensive Coverage Doesn’t Cover in Florida Hurricanes

Honest talk: Gaps exist.

- Wear/tear pre-storm (e.g., existing rust)

- Neglect (parked in known flood zone without mitigation)

- Earth movement (sinkholes, landslides)

- Collision-style damage (if you hit something—needs collision coverage)

Pitfall: Insurers deny if you drove through floodwaters. Park high ground next time.

Florida Hurricane Vehicle Damage Claim: Step-by-Step Process

File promptly—deadlines often 1 year from hurricane landfall (varies by policy). Safety first.

Step 1: Ensure Safety & Initial Assessment

- Move to safe spot if drivable.

- Check for leaks, fire risks, airbag deployment.

- Tow if needed—comprehensive often covers.

Tip: Never drive flooded cars—electrical failure risks stranding you.

Step 2: Document Everything Thoroughly

Photos/videos from all angles:

- Exterior dents/scratches

- Interior water lines/mud

- Odometer, VIN

- Underhood/engine bay

Pro move: Timestamped pics prove pre-adjuster condition. We’ve won supplements with these.

Step 3: File the Claim Immediately

Call your agent/app. Provide:

- Policy number

- Hurricane details (e.g., Milton impacts)

- Damage description/photos

Expect claim number instantly. Rental approval often follows.

Step 4: Schedule Adjuster Inspection

They inspect within 48–72 hours post-storm. Be present. Point out issues politely.

Our role: At Pro Car, we provide detailed estimates beforehand—adjusters respect I-CAR certified shops.

Step 5: Review Estimate & Approve Repairs

Compare to our Free Estimate. Negotiate lowballs.

Step 6: Handle Supplements for Hidden Damage

Teardown reveals more (e.g., frame rust from flood). Submit photos—we advocate.

Step 7: Complete Repairs & Close Claim

Direct billing means no out-of-pocket beyond deductible. We coordinate rentals.

Common Hurricane Auto Claim Florida Pitfalls to Avoid

Storms bring scams and shortcuts. Watch for:

- Lowball estimates (insurers undervalue labor/parts)

- Rushed “like-new” promises from pop-up shops

- Total loss push when repairable (we fight undervalued ACVs)

- Rate hike fears (rare for comprehensive—Florida rules protect)

Example: Orlando driver post-Helene got a $15K total loss offer. Our appraisal proved $22K ACV—full value paid.

Supplements in Hurricane Vehicle Damage Claims: Why They Matter

Initial estimates miss 40–60% of damage, per our experience. Supplements add costs for hidden issues.

When needed:

- Flood: Wiring harness corrosion

- Hail: Paint cracks under dents

- Debris: Misaligned frames

Process:

- Teardown during repair

- Photos + OEM part quotes

- Submit to insurer (90% approval rate with pros)

We’ve secured $5K+ supplements for Broward flood victims.

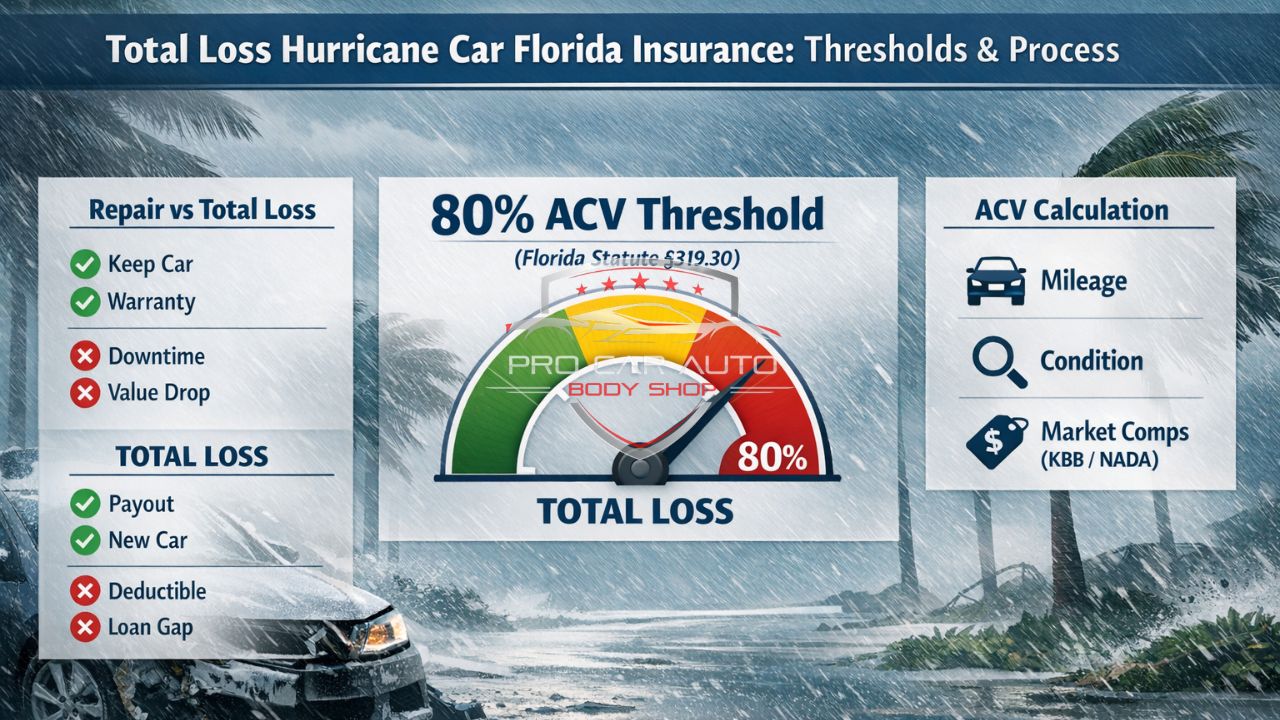

Total Loss Hurricane Car Florida Insurance: Thresholds & Process

Florida Statute §319.30 defines total loss if repairs ≥ 80% of Actual Cash Value (ACV).

| Repair vs. Total Loss | Pros | Cons |

| Repair | Keep your car; lifetime warranty from us | Downtime (2–6 weeks); future value drop |

| Total Loss | New car payout (ACV minus deductible) | Gap insurance needed if loan > value; tax/title hassles |

ACV calculation: Mileage, condition, market comps (KBB/NADA).

Fight undervalues: We provide market data. Post-Milton, we upped a Tampa truck’s ACV by 25%.

Hail, Wind, Debris Hurricane Auto Claim Florida Specifics

Hail: PDR fixes 80% without paint—saves time/money.

Wind/Debris: Frame machines straighten unibodies precisely. ADAS recalibration essential post-impact.

Flood: Assess electronics first—restorable if acted fast.

Pompano Beach Hurricane Repair Insurance Help: Why Local Expertise Wins

Our Pompano Beach HQ at 1705 Dixie Hwy sees statewide traffic. From Miami to Jacksonville, we handle hurricane flood damage car insurance Florida claims seamlessly. I-CAR/ASE certified techs use OEM parts.

Will a Hurricane Claim Raise My Rates in Florida?

Usually no. Comprehensive claims for hail/hurricanes are “no-fault”—insurers can’t hike for weather. Confirm with your agent.

Choosing the Right Shop for Hurricane Repairs: Your Rights

Florida Statute §626.9743: You pick the shop. Insurers suggest, but can’t force.

Vet shops: Certifications, reviews, direct billing.

FAQ Section

Does insurance cover hurricane damage to my car in Florida?

Yes, via comprehensive coverage for wind, hail, flood, debris—not liability/PIP.

What if my car is flooded—is it covered under hurricane flood damage car insurance Florida?

Yes, if sudden/accidental. Document water lines; supplements catch hidden corrosion.

How do I file a hurricane car insurance claim in Florida?

Safety first, document, call insurer ASAP, get adjuster—follow our 7 steps above.

Does comprehensive coverage cover hail damage from hurricanes in Florida?

Absolutely—PDR often fixes economically.

Will a hurricane claim raise my insurance rates in Florida?

Rarely for comprehensive; it’s an “act of God.”

What’s the total loss threshold for hurricane car Florida insurance?

80% of ACV per §319.30— we help appraise fairly.

Can I choose my own repair shop for Florida hurricane vehicle damage claim?

Yes, per §626.9743—insurers can’t dictate.

How do supplements work in hurricane vehicle damage claims?

Post-teardown adds for hidden issues; photos prove need.

Does insurance cover wind and flying debris in Florida hurricanes?

Yes, under comprehensive—frame work common.

Serving Pompano Beach and statewide: How can Pro Car help my hail dent repair?

Free estimate, PDR experts, claim advocacy—call (561) 372-4547.

What’s the timeline for hurricane car damage insurance Florida claims?

Filing: days; repairs: 2–6 weeks; we expedite.

Is ADAS recalibration covered after hurricane structural damage?

Yes, if damage-related—our certified techs handle it.

Conclusion

Hurricanes test Florida drivers, but with comprehensive coverage, solid documentation, and expert help, you can navigate claims, secure supplements, avoid total loss traps, and drive away restored. Key takeaways: Get comprehensive, file fast, choose your shop, and demand fair ACVs.

Pro Car Auto Body Shop has guided hundreds through post-storm recoveries—from Miami floods to Jacksonville winds. We serve all Florida with I-CAR certified repairs, direct billing, and fierce advocacy.

Ready to start?

Call (561) 372-4547 now for your free hurricane damage assessment.

Email info@procarautobodyshop.com.

Visit 1705 Dixie Hwy, Pompano Beach, FL 33060.

No comment